Introduction

Dollar cost averaging, often referred to as “DCA”, is the technique of investing a fixed amount of money at regular intervals regardless of market conditions. Most investors know that trying to “time the market” is never a good plan (and not possible on a consistent basis). Periodic interval investing has become the prevailing wisdom and is common advised investment technique. It has been touted as a safe, disciplined way to invest for the future. As a result, many people elect to dollar cost average a financial windfall rather than invest the lump sum all at once.

When I retired, I sold my house that took me twenty years to pay off and moved to a state with more sunshine….. and no state income tax. At closing, my attorney handed me a check for several hundred thousand dollars. Despite the “prevailing wisdom” above, I immediately invested the lump sum in a brokerage account and bought a total market index fund. I avoided dollar cost averaging because historical market data show that being fully invested sooner usually yields better results. Let’s look at the math…. and we’ll see how it worked out for me at the end of the post.

We’ll review the basics dollar cost averaging, the risks associated with it and the key market statistics that give lump sum investing the advantage.

Understanding Dollar Cost Averaging

As noted above, DCA is the technique of investing fixed amounts of money at regular intervals ignoring recent market trends. This type of investor doesn’t try to time the market…. an impossibility. The idea is to spread stock purchases over time. As a result, more shares are bought when the prices are low and fewer shares when prices are high.

This theoretically becomes advantageous by lowering the average cost per share over long periods of time. It also reduces the risk of investing a large lump sum right before a market crash, a real fear for an aspiring retiree. The technique gained popularity among risk-adverse investors who fear losing a significant portion of a lump sum investment in a market downturn.

Let’s take a look at a theoretical example. You have $12,000 to invest and decide to invest $1,000 every month for twelve months rather than investing all $12,000 as a lump sum. In month 3, the market dips and your $1,000 buys more shares. In month 8, the market rallies and your $1,000 buys fewer shares. Over time, this situation can smooth out the volatility of the market and potentially gives you a better average price than trying to “time the market.”

Superiority of Lump Sum Investing

Lump sum investing is exactly what it sounds like and is the opposite of dollar cost averaging. When a lump sum investor receives a monetary windfall, they immediately invest the entire amount into the market all at once. (Gasp!) What if the market crashes next week?!

In 2023, Vanguard published a study compared lump sum investing to dollar cost averaging and determined that investing the lump sum was the right answer 68% of the time over various periods. Why? There are a few reasons. The most important reason is that market tend to rise over time. This is true at all time intervals. In fact, day to day, the market rises 53% of the time. Weekly 57% of the time. Monthly 62% of the time and annually 73% of the time. Overall rolling decade-long periods, the market went up 88% of the time.

In 2023, Vanguard published a study compared lump sum investing to dollar cost averaging and determined that investing the lump sum was the right answer 68% of the time over various periods. Why? There are a few reasons. The most important reason is that market tend to rise over time. This is true at all time intervals. In fact, day to day, the market rises 53% of the time. Weekly 57% of the time. Monthly 62% of the time and annually 73% of the time. Overall rolling decade-long periods, the market went up 88% of the time.

Money sitting on the sidelines misses the gains from these probable increases. In addition, money sitting of the sidelines decreases in value by the rate of inflation. This represents the lost opportunity costs of dollar cost averaging. The compounding affect during the investment period also contributes to the gains and the technique superiority.

Proponents of dollar cost averaging hope to avoid the coming crash by easing their way into the market. However, they fail to realize that, by waiting, they may miss a market rally. As noted by the percentages above, it is more likely the market will rise than fall. In addition, they fail to realize that the value of the money on the sidelines is being eroded by inflation.

The Bottom Line

Here’s the bottom line. If the market declines over your investment period, dollar cost averaging wins. In a rising market, lump sum method wins. If your think you can identify a declining market, you’re wrong. No one knows what the market will do next week, next month or even next year. We can only use historical data and statistics to make a decision.

It turns out that, when taking the likelihood of a rising market (ranging from 53% to 88%), opportunity costs and inflation, investing a financial windfall as lump sum is the right answer 68% of the time. Investors that are particularly risk adverse will tend to focus on the 32% of the time that lump sum investing was the wrong choice. However, even when it was the wrong choice, your investment will recover at some time in the future. The market always goes up….. eventually.

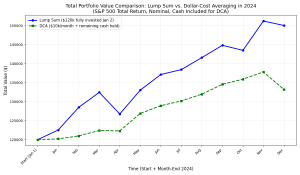

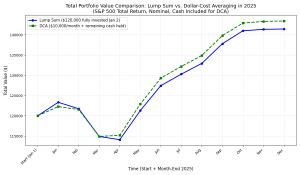

Here are two graphs that compare lump sum investing and dollar cost averaging for the last consecutive two years, 2024 and 2025. In each case, $120,000 was invested. For the lump sum investment, $120,000 was invested into the S&P 500 on January 1st. For DCA, $10,000 was invested into the S&P 500 at the beginning of each month beginning on January 1st. The results were adjusted for that year inflation. The first graph represents the results for 2024; the second graph is for 2025.

Dollar Cost Averaging (Green) vs. Lump Sum Investing (Blue), 2024

In 2024, the market steadily climbed without any official “market corrections” (10% drops). There was, however, a dip of about 4.1% in April. Lump sum investing in that year, represented by the blue line, clearly beat dollar cost averaging. In fact, lump sum investing generated $6,943 (or 5.8%) more than dollar cost averaging. Graphs for any given year would look similar 68% of the time. Some years would show a large difference. Others, a smaller difference.

The following year, the story was a little different. In April of that year, the market fell approximately 19%, just shy of the 20% that defines a “bear market.”

Dollar Cost Averaging (Green) vs Lump Sum Investing (Blue), 2025

The graph above compares lump sum investing (blue line) and dollar cost averaging (green line). In this case, dollar cost averaging slightly beat lump sum investing. This was a result of the significant market decline in April 2025. DCA resulted in $1,975 (or 1.6%) more that lump sum investing. Graphs for any given year would look similar 32% of the time. Some years would show a large difference. Others, a smaller difference.

When Does Dollar Cost Averaging Make Sense?

Dollar cost averaging makes the most sense when with money available for investing only comes to the investor periodically and in relatively small amounts. This is the situation when you contribute $250 a month to your Roth IRA or 3% of each paycheck into your 401K. The reason you invest these relatively small amounts every month or with every paycheck is that that is all you have to invest at the time. You are actually lump sum investing all of the available money at the time, but since we do it repeatedly, we think of it as dollar cost averaging.

I’m a huge fan of “dollar cost averaging” in this fashion and automating the process. I would also recommend that a significant portion of future salary increases be automatically invested the same way.

Author’s Conclusion

If you’re lucky enough to receive a financial windfall, you’ll have some decisions to make. If you need the money in the short term (1 to 3 years), I wouldn’t invest the money into stocks at all. Regardless of whether the money is dollar cost averaged into the market or invested as a lump sum, one to three years might not be long enough to recover from a significant market downturn. If this money was needed for my kids college tuition or some similar important need, I might invest it in a bond fund or bond ladder. If I needed it for a car purchase in the next six months, I’d stick the money in a savings account.

As long as I don’t need the money in the next three years, I’ll invest the lump sum, regardless of the amount, into a total market index fund such as VTSAX or VTI. When the market goes up (68% chance), I’ll pat myself on the back and remind my wife that she is married to the next Warren Buffet.

What Happened with My Lump Sum Investment?

So, what happened with my lump sum investment? As noted above, in January 2024, I invested the proceeds from the sale of my home as a lump sum investment. By April 2024, Dow Jones Industrial Index had dropped more than 2,000 points or 5%. Oops!

I had two options. Option one was to double up on my antacids and do nothing. Just sit and wait for the market to recover. Remember? The market always goes up… eventually. In fact, three months later, the market recovered and I was back where I started. Since I didn’t need the money immediately, there was “no harm, no foul.”

Option two (my choice) was to sell my holdings in VTSAX after the 15% drop! (I can hear the gasps.) I did not sell out of panic or fear. Instead, I did it to take advantage of a technique called “tax loss harvesting” (see future posts) by immediately buying VOO, Vanguard’s S&P 500 index fund. VOO and VTSAX are similar (although not identical) mutual funds that typically rise and fall together. So, three months later, VOO also recovered.

Selling VTSAX, after the dip, “locked in” in the losses, at least on paper. These loses, called “capital losses, will offset future “capital gains” when I sell funds that have increased in value to fund my retirement, This, in turn, will decrease the taxes I pay in the future.

The Value of Hindsight

Dollar cost averaging back in January 2025 would have been the better choice, but only in hindsight. However, if I had dollar cost averaged into the market over a year, I would not have the opportunity to take advantage of tax loss harvesting and save on future taxes.

In the absence of hindsight, like in the real world, I would recommend lump sum investing a financial windfall. It’s the right decision, for me, 68% of the time. You’ll have to access your own risk tolerance and ability to stomach a significant market downturn and hold on for a wild ride.